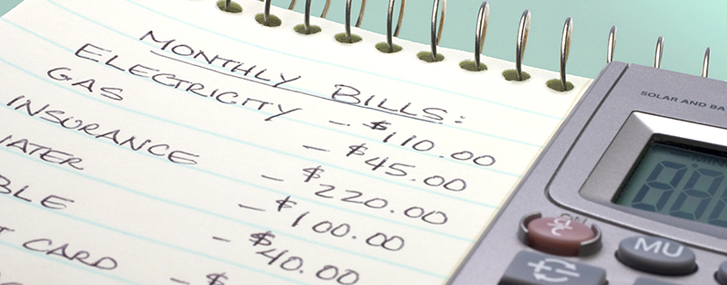

How to spending plan in 7 basic steps

3. Compute your earnings

If you have a fixed quantity of money you receive routinely (for example, a wage), then add your incomes over the month and plug that into your spending plan. If your income differs from month to month, use the lower series of past month-to-month earnings. For instance, if your regular monthly take-home income (post-tax and other reductions) varies from $2,500 to $5,000, then create your budget plan as though you can just expect $2,500 each month. If you wind up with more money than you expect, you can wait or utilize it where it’s needed.

In addition, do not ignore taxes. If you’re a W-2 worker, your net pay, or “take home pay” has currently had taxes subtracted as soon as it’s been deposited into your account. Nevertheless, if you’re a specialist or self-employed, since your earnings may be gross pay, or total earned with no taxes gotten, make sure to set aside a portion as you will need to pay taxes on it in the future.